This is a journal entry about controlling your expenses and understanding how your bills effect your income through time.

An individual’s potential is measured by their ability to balance what is needed vs. what is wanted. This post is about applying self-discipline to achieve a goal that can be commonly realized using very simple arithmetic. Problem is… most people simply do not look into the details.

When I was younger (age 10-13), I went through a period where I had been prescribed a medication, which led to a minor weight gain. Just like any other kid, I favored soft drinks, frozen foods and chocolate; however, I was active enough that my metabolism could keep up. After receiving a prescription, my metabolism had slowed, and I learned what it was like to attend school with a bunch of bad kids. It was incredible how subtle changes in appearance can turn life-long best friends cold.

The summer between middle school and high school, my parents pulled me from one district and placed me into private school. I made a solid point to lose any and all weight I had added.

Want to see something hilarious… here are some yearbook photos.

2003

2005

I totally removed chocolate and soda from my diet, and I rode my bike for miles every day, all summer long. I also continued to play soccer from age 6-18 every year and joined the track team. Luckily, I had growth on my side.

Funny thing though, I actually developed a complete distaste for sweet foods. This did not happen overnight. But over the course of a year, cravings completely disappeared, and I was no longer able to tolerate sweet or buttery foods. Still to this day, I can’t eat half the things I enjoyed then.

I mention this, because finance is no different. If you find yourself struggling financially, you could almost certainly change something about your spending habits, regardless of your income bracket. I know… sounds untrue, but it’s completely valid.

Let me pause here… if you haven’t seen it, go watch Fight Club. Story and plot aside, that movie is filled with useful messages to help discern needs vs. wants.

Let me pause here… if you haven’t seen it, go watch Fight Club. Story and plot aside, that movie is filled with useful messages to help discern needs vs. wants.

Conversation resumes…

Financial success isn’t defined by the amount of cash you have, it’s defined by the ability to make transactions happen (cash flow). The economy isn’t one big fund of cash, it’s a community engaged in transactions and the math is so, sO, SO simple.

For example… many of my subscribers might hold a mortgage or a student loan and think it’s best to pay down debt as quickly as possible in order to get ahead. This concept is flawed and I’m going to explain why…

Imagine you purchase a home. The borrowed amount is $208,000.

You’ve scored a great interest rate at 2.875% for a 25-year loan.

Monthly principal and interest are $972.89.

Monthly taxes and insurance are $523.82.

Total monthly payment is $1,496.71 for 25 years.

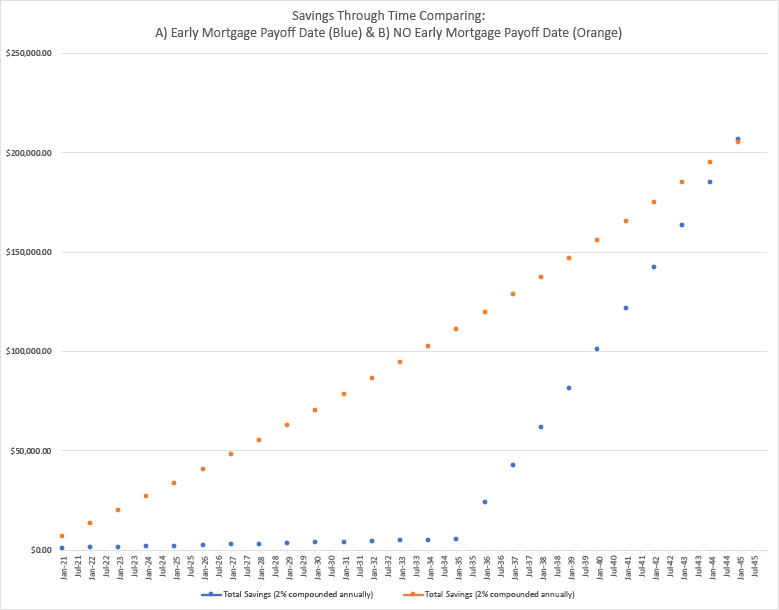

A table is shared below, which was used to model column B against column C.

Column B calculates an overpayment of $500 per month to achieve an early payoff in March 2035. You will be 15 years older.

Column C calculates no overpayment and achieves a payoff in December 2045. You will be 25 years older.

A number of assumptions are made in the model.

- Salary never increases or decreases through time. In reality, income will be greater over the course of 25 years.

- Bills never increase or decrease through time. In reality, you have control of your spending habits.

- Taxes and insurance are fixed through time. In reality, taxes and insurance costs will increase substantially over the course of 25 years.

- All savings are invested to generate modest gains at 2% compounding annually.

NOTE*** For all assumptions, inflation is on your side as long as your money is invested and not held by a bank. See here: https://peldspar.com

Methods:

The formula used to calculate gains compounded annually is A=P(1+r/n)^nt.

A – final amount,

P – initial principal balance,

r – interest rate,

n – number of times interest applied per time period,

t – number of time periods elapsed

In excel for cell I15, this formula is expressed by I15=FV(0.02,1,0,(H15+I3)*-1)

Key takeaways:

- Instead of making incremental or irregular overpayments, it is far better to pay the minimum balance due. In only 5 years, you will have saved $40,265 of your own money. If you attempted to overpay your loan, you will have only $1,792 and you would have given -$38,473 directly to the bank to use and invest for their own financial gain. The $40,265 is leverage that you own. You can use this cash to press your advantage to build a far greater savings account 20 years from now.

- If you decide to make regular overpayments to shorten the life of your loan, you will be debt free on March 3035. However, you would only have $4,923 in savings and you would still need to pay your insurance and property taxes. We assume these costs have not risen and are fixed at $523.82; however, in all likelihood, these amounts would have risen by >20%. Contrast this with your financial position if you had never overpaid. You would have roughly $110,599.83 in savings and are living comfortably because you are in control of your cash flow!

- You can see that over the course of 25 years, an overpayment schedule will inevitably yield more cash; however, you would have lived a significant portion of your life with little money set aside to use on hobbies, etc. This has a lasting psychological effect where people tend to overspend when they realize they are “debt free.” It’s also much harder to discipline yourself to stow away excess income later in life, but I will not make these assumptions. In reality, they still have a tax and insurance obligation. You’ll soon realize that your home mortgage remains an annual subscription even when the loan is paid off.

Conclusions:

When people describe “good debt,” they are literally referring to mortgages and affordable car payments. This is money that the bank is giving you because you’ve proven to be financially responsible. When people grant you a loan, it means you have the advantage and can use your control to build a more robust savings account at a faster pace. Paying off the loan more quickly, defies the opportunity of receiving the loan in the first place. This “good debt,” is a cash injection that allows you the opportunity to preserve and grow savings. The reality is, 2% is a very unlikely growth rate. Actual savings would be accruing at a significantly higher percentage. Do not castrate yourself and teeter on the edge of debt for 15 years when you don’t have to. Just pay the minimum and understand how to balance your income vs. expenses.

When people refer to “bad debt,” they are referring to luxury or hobby items that are not necessity. In most cases, people tend to choose a path that is consistent with column B. At some point, these people might consider indulging in a fancy car, a boat or other. Literally any purchase that would fit the bad debt category should never be financed. Bad debt items should only be purchased when the savings in your investment account is 10x greater than the cost of the hobby or luxury item you aim to buy. This allows you to keep your leverage and never puts you in danger of losing a positive monthly cash flow.

There is a lot of material to discuss related to these conclusions. Everything from product pricing to interest rates. Simply understand and ask yourself when it’s time to indulge… would I rather live comfortably with the cash -or- live uncomfortably with the asset?

Please leave comments or ask questions, i’m here to help.

“The things you own end up owning you.” – Tyler Durden

Great article on a concept many people struggle to clearly understand.

Of course, thank you Matt! The model becomes even more interesting as you apply different variables. Wanted to keep this model simple for the time being.